Harnessing carbon markets for methane mitigation

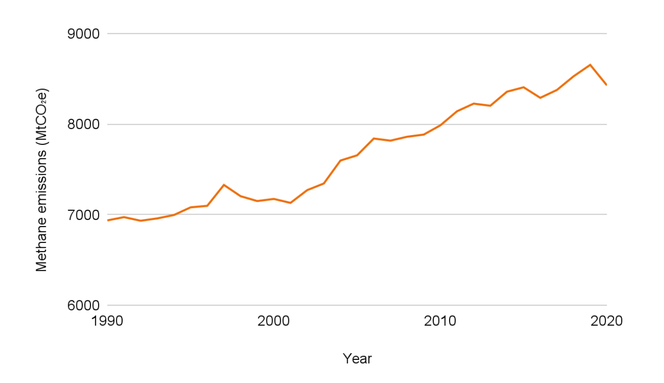

Methane is the second-most abundant greenhouse gas (GHG) after carbon dioxide (CO2), accounting for around 20% of global GHG emissions.¹ Global trends in methane emissions indicate that this GHG has been rising at an accelerated rate since the early 2000’s (Figure 1).

Methane is a short-lived GHG which means that activities that abate or avoid methane emissions have potent near-term climate impacts. This effect has been recognized by the Global Methane Pledge to reduce global methane emissions by 30% by 2030 relative to 2020, launched at COP26 and endorsed by more than 150 countries.

Figure 1. Global methane emissions exhibit an increasing trend. Data from CAIT, available until 2020.

Within BeZero’s sector-classified database of projects in the voluntary carbon market (VCM), nearly 16% of projects have activities that primarily abate or avoid methane emissions. These projects can tackle waste emissions through landfills, biodigesters, or industrial methane emissions such as fugitive gas leaks or coal mine methane. Some nature-based projects tackle agricultural methane emissions through activities that reduce enteric emissions from cattle or via water management in rice paddy fields. Many other projects tackle methane emissions through their secondary activities or carbon pools.

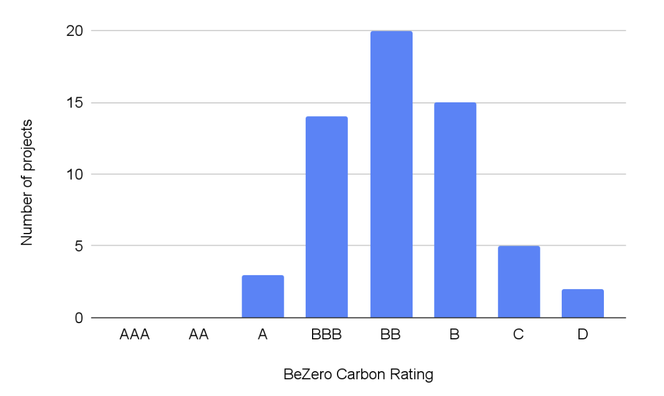

BeZero Carbon has rated 59 methane reduction projects across 16 countries, and we observe a dispersion of credit quality across six letter ratings on our eight-point scale (Figure 2). Differences in credit quality are driven by project-level analyses across five risk factors where the variable roles and uses of carbon finance, regional barriers, common practice, and approaches to carbon accounting are considered. For example, for each project, we examine traits such as whether direct measurements or models are applied, global warming potentials, and whether methane oxidation factors are accurate, among others.

Figure 2. The distribution of BeZero Carbon ratings across 59 methane reduction projects.

Recently, there has been a surge in innovative approaches and technologies aimed at mitigating methane emissions across various sectors. From the development of new methodologies such as those related to decommissioning coal mines or orphaned oil wells to novel satellite products, the market for methane projects is undergoing a transformative shift. These advances are timely as the VCM strives for quicker and higher impact. For example, with the imminent release of market labels such as the ICVCM Core Carbon Principles, several categories of methane reduction projects are already fast-tracked for internal assessments.

Emerging techniques are enabling greater resolution and accurate quantification of methane emissions. At BeZero, we have extensive ratings coverage for methane reduction projects, leveraging our partnerships and in-house expertise to independently assess and monitor the efficacy of their climate impacts.