Cooking with quality: improving cookstoves

Here are some key takeaways

The Cookstove sub-sector offers a globally significant opportunity to reduce greenhouse gas emissions. However, to date, there have been concerns surrounding the quality and integrity of these projects.

Methodologies and standards are continually evolving in response to these criticisms; but the onus is on projects to adopt these improved measures and show transparency in their reporting.

There is a demand for high quality cookstove credits and, if the price is right, there is no reason why projects cannot deliver this.

Contents

- Introduction

- Standards developments

- Project reporting

- Additionality

- Carbon accounting

- Next steps

- Conclusion

Introduction

Roughly one-third of the global population, primarily in the global south, relies on biomass or highly polluting fuels for household cooking.¹ The greenhouse gas emissions from burning non-renewable biomass for cooking equate to approximately 2% of global emissions, putting the climate impact of household cooking on a plane with the global commercial aviation industry.², ³ These practices are also cited to be responsible for more than 25% of global black carbon emissions⁴, which are linked to millions of premature deaths every year.⁵ A switch to clean cooking is a necessary climate action, and carbon finance could be fundamental to enabling this transition.

There are several reasons driving the prevalence of polluting cooking practices, all of which are technically surmountable with interventions backed by climate finance. The main barriers to the adoption of clean cooking techniques are financial constraints, access to fuels and technologies, awareness of the benefits from clean cooking, linked with inexorable ties to traditional methods, and logistical issues, including reaching last mile users and ensuring quality production. There are feasible solutions to all of these barriers; using carbon finance to help implement marketing campaigns and distribute quality, affordable cookstoves. However, despite their clear value, improved cookstove projects are increasingly coming under fire.

This is primarily due to a lack of transparency driving a lack of trust, raising integrity concerns and questioning quality in the market. Our analysis finds that common issues are to do with additionality - driven by uncertainty over how important carbon finance is to the project’s operations, and with over-crediting - driven by uncertainty in projects’ emission reduction calculations. These problems are pervasive across the projects we have rated in this sub-sector, and, based on literature and market commentary, appear to be systematic across the sector group. The issues are routinely flagged in our ratings and have also been discussed in detail in our published methodology for rating Household Devices projects.

Rather than shining a torch on problems that are already under the spotlight, the aim of this piece is to highlight that there is a spectrum of quality even in this sector, and that it can be possible to purchase reliable credits from an improved cookstove project.

Standards developments

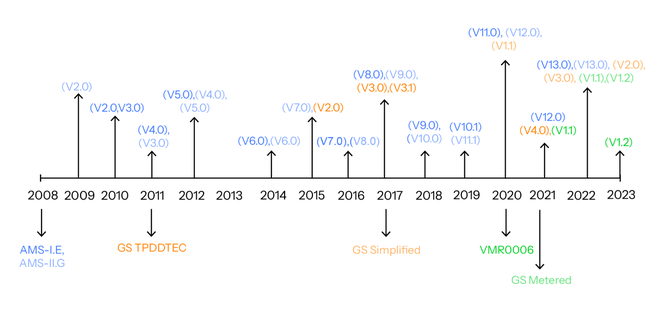

In 2007, the Clean Development Mechanism (CDM) pioneered the introduction of improved cookstove projects to the VCM. This was through the development of two small-scale methodologies that were designed to target both fuel-switch and improved efficiency projects. Since then, we have seen the rapid and continual growth and revision of cookstove methodologies (Chart 1).

Chart 1. A timeline of the major cookstove methodologies with key version updates.

Newer methodologies have generally improved on previous metrics and measures to help ensure quality. For example, the Gold Standard Metered & Measured methodology requires direct measurement of energy or fuel consumption. Stove Use Monitors (SUMs) or other metering technologies must be in place to monitor usage of all project devices in order to inform both baseline and project emissions. This reduces sampling risks and helps to eliminate bias, enabling data-driven proximations. By contrast, other earlier methodologies in the sector allow projects to adopt 100% usage rates based solely on the survey question ‘do you use the project cookstove?’ - an assessment that is subject to significant uncertainty and reliability issues.

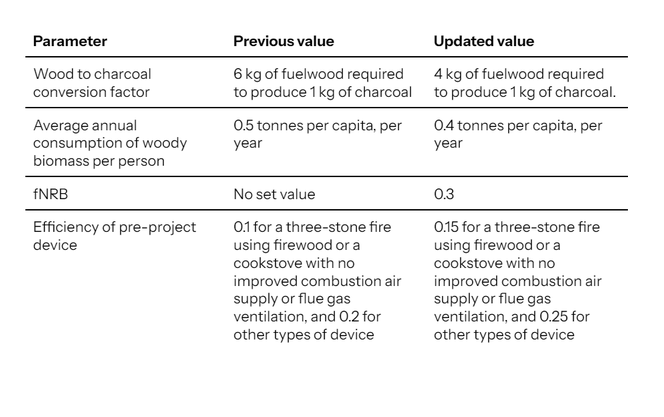

Similarly, methodologies are generally improved upon as they are revised, aiming to confer more conservative accounting measures. For example, the latest version of the GS-TPDDTEC methodology has excluded use of the ‘first-of-its-kind’ analysis to demonstrate additionality. More recently, the latest version of the Verra VMR0006 methodology includes additional procedures to account for uncertainty in fNRB and relies on updated default values from TOOL 33 (Table 1). Our analysis has previously identified that both first-of-its-kind assessments and fNRB uncertainties are key drivers of lower credit quality. Therefore, we view these changes to be both necessary and progressive, acting to improve carbon efficacy.

Table 1: Updated default values under TOOL33.

This suggests that accreditors and methodologies are trying to respond to market feedback, iron out uncertainties, and develop more accurate approaches to determine emission reductions. Although this provides an encouraging outlook, it is important that projects actually transition to these improved standards. For example, since its release in October 2021, no credits have been issued under the GS metered methodology (although this is in part due to a slow certification process). Likewise, the current default value of 30% fNRB has seldom been applied, with most projects using TOOL30 to yield higher and less conservative values of fNRB.⁶

Project reporting

Improving standards and methodologies is one half of the equation, but there is also an onus to improve project reporting, making explicit where values have been sourced from, how activities have been conducted, and where carbon finance has been channelled. In particular, when adopting less conservative parameters, there needs to be a detailed explanation as to why this decision has been made.

One way to achieve this and build trust in the market is through greater transparency. At present, standards bodies generally require a minimum level of public reporting and there is no obligation for projects to disclose more information than required. In fact, there is often a disincentive for this as it can require greater time and monetary resources. Moreover, as a number of cookstove projects operate as a competitive business, there is also the risk of unwillingly or unwittingly publishing proprietary information. The challenge is therefore striking the balance between a minimum and sufficient level of reporting, and we would argue that this is both feasible and necessary to provide greater transparency without increasing vulnerability.

Through our engagement with project developers and various site visits, we are aware that there can be a wealth of information collected by individual projects that is not available in the public domain. For example, household-level data is generally well collected, including parameters such as location, fuel expenditure, and cooking habits. Projects involved in fuel distribution are also capable of collecting data on ex-post fuel consumption, providing a clear proxy for usage rates. This level of granularity is essential for accurate credit issuance, yet this data can often be poorly transcribed. Whilst not essential or appropriate to publish all of this information, it should be necessary to disclose what and how such data has been collected and how this feeds into emission reduction calculations.

Providing evidence of data-driven conclusions also reduces the risk of reporter bias. Conflicts of interest can be exacerbated when entities that benefit from maximising credit issuance conduct their own monitoring - essentially marking their own homework. Improving transparency across all aspects of carbon accounting can act to counter these biases and level allegations. As in an exam, show your working, otherwise there will be rumours of cheating.

So what does a quality cookstove project look like? Here we focus on the two risk factors in the sub-sector that are subject to the most uncertainty: additionality and carbon accounting.

Additionality

In terms of additionality, a project should be able to clearly identify how it has overcome pre-existing barriers to adoption and distributed stoves to end-users who would have otherwise relied on more polluting technologies for the duration of the crediting period.

Common barriers to clean cooking include financial constraints, a lack of awareness, ties to traditional practices, and logistical issues. Improved cookstove projects must be able to elicit which of these barriers they are surpassing, and how they are doing this, as well as demonstrate that they were otherwise an inhibiting factor to end-user clean cooking. Below is a snapshot of what projects can do to demonstrate additionality. It is not intended to be exhaustive.

Financial barriers: Households may not be able to afford improved cookstoves or clean fuels and so rely on traditional, polluting cooking practices. Carbon finance can be used to subsidise stoves and fuels, or distribute them free of cost*. Investment analyses should be published to demonstrate key metrics, such as the level of discount, the stove manufacturing cost and retail price, fuel prices, and project costs.

Awareness barriers: Households may not be aware of the benefits of clean cooking or of the issues regarding traditional practices. Carbon finance can be used to fund marketing and awareness campaigns, host events and demonstrations, or pay renowned and respected members of the community to educate and inform. Details of the capacity of these campaigns should be reported, including the frequency, target audience, results, and expenditure.

Technical barriers: Households may be tied to baseline practices for traditional or technical reasons. Projects can initially prescribe deliberative methods, incorporating group-based dialogue and processes of participation to elicit cultural preferences and values. An understanding of household needs and perceptions can be used in stove design to ensure that it meets the expectations of end-users and is adopted.

Operational barriers: Households may not have access to clean cooking technologies. Carbon finance can be used to implement new supply chains and distribution lines to reach last mile users or to enter new markets that are otherwise dominated by traditional cooking appliances. The locations of the targeted populations should be made clear, as well as the steps taken to implement these measures, with particular regard to the role of carbon finance.

*We do however note the risk that free distribution can result in lower perceived values, leading to poor maintenance and usage rates. There is also risk to project longevity as a self-sufficient market cannot be established.

Demonstrating how carbon finance has been used to overcome barriers to clean cooking should be a straightforward task, yet we still find it to be routinely underreported. For example, less than 10% of projects BeZero have rated in the Cookstove sub-sector provide an investment analysis to demonstrate how and where carbon finance has actually been utilised. This is the essence of additionality, as if projects can successfully operate without carbon finance, then they are essentially a conventional business and inherently non-additional. In this aspect at least, it is likely that transparency is the limiting factor in credit quality, thus leaving a clear fix.

A more difficult aspect is demonstrating how additionality is maintained over the project’s crediting period. A fundamental assumption is that households would not have progressed to a cleaner cooking practice without the project’s intervention; an assumption that is seldom supported by evidence and data. One reason for this is that the methodologies treat additionality as a binary. Projects in locations with low penetration rates of improved stoves, small projects in certain locations, or projects using specific technologies are automatically considered additional. All other projects must demonstrate that they would not have gone forward without carbon revenues using simplified additionality tools, which have been criticised for being inaccurate.⁷

As was observed in our site visits, projects do have access to sales records and information of each end-user, meaning they are capable of documenting the baseline stove in each household at the time of ICS adoption. This is a useful point in time assessment of additionality, but it is a static assessment and therefore limited in its ability to inform the counterfactual or baseline period.

Whilst there are no perfect solutions, given the obvious limitations in measuring a hypothetical, there are various approaches that can be taken to reduce uncertainty. For instance, regular reports on the state of the local market could act as a useful additionality benchmark. If the project stove maintains a greater efficiency (based on ISO Tiers), quality, or lower price than other available stoves, it may be assumed that without the project intervention there would be no alternative for end-users (although the baseline technology may still have improved to a level lower than the project technology).

There is also the option to monitor control households, observing whether households representative of project end-users but beyond the project boundary transition to clean cooking in the absence of any intervention. Of course there are limitations with this approach, as finding a perfect control would mean that they are eligible for the intervention and should therefore be targeted by the project. Other options could be to use national or subnational data on cooking trends to serve as an indicator for the baseline, introducing adjustment factors where necessary to capture any changes.

It is outside the scope of this piece to detail all aspects of additionality, and beyond the jurisdiction of a ratings agency to be providing a perfect set of guidelines for projects to adhere to. However, besides serving as a thought piece, this segment should hopefully highlight that a lot of additionality issues are a result of opacity in project reporting. Quality is dependent on trust, and trust is dependent on transparency. A fix as simple as publishing more information could be a first step in ensuring confidence in project additionality. This should also filter down into the current nebulousness of carbon accounting.

Carbon accounting

In terms of carbon accounting, it is unlikely that any project can be 100 percent accurate in its emission reductions, given that credits are generated against a counterfactual baseline (as discussed above). However, there are best practices and conservative measures that can be taken to reduce uncertainty, avoid egregious over-crediting, and instil trust in the market. Again, the factors outlined below are by no means exhaustive, but rather serve as an example of what best practice may look like.

Baseline: A critical component of carbon accounting is selecting an appropriate baseline. In the case of cookstove projects, best practice would require individual baselines for each end-user so that there is household level crediting, or at least selecting a modal baseline predicated on these data. Individual baselines would capture the prior cooking habits of each end-user, including stove technology, fuel type, and consumption. As such, emission reductions would represent actual differences in fuel consumption and efficiency for each household, rather than relying on sweeping generalisations of baseline habits that do not capture population heterogeneity.

fNRB: The fraction of non-renewable biomass (fNRB) is generally the major parameter in emission reductions and also subject to the most uncertainty. Values should be based on the best available data at the time. Currently these are derived from the MoFuSS and WISDOM models, which rely on a more robust approach than previous default values, incorporating elements such as biomass regrowth and land use heterogeneity. Methodological requirements to adopt a flat 30% fNRB would also counter the risk of over-crediting and likely be a particularly conservative implementation.

Emission factors: The actual emissions released from baseline and project fuel consumption need to be accurately accounted for to ensure reliable crediting. Both upstream and point of use emission factors need to be captured to realise the net climate impact of the intervention. These values should be sourced from the most up-to-date studies and routinely updated, both prospectively and retrospectively, rather than relying on outdated or default values.

Usage: The usage rate applied by projects and the monitoring techniques used to determine this value can greatly influence net emission reductions. Stove use monitors (SUMs) and metered technology should be used to track real-time usage where feasible. This can be partnered with data on fuel purchases where available. Where metering is not possible, long-term longitudinal observations should be conducted across representative samples that sufficiently capture the heterogeneity of end-user populations and environments. Exactly how this data is obtained and incorporated into emission reduction calculations should be made transparent.

It is beyond the remit of this piece to delve into every aspect of carbon accounting, as each could rightly warrant its own thesis. Indeed, there is a wealth of literature already in existence describing problems and solutions across these factors, some of which have been discussed in more detail in our own publications.

Instead, as with Additionality, the aim is to show that there are relatively simple (theoretically perhaps rather than practically) measures that can be adopted to derive more accurate estimates of emission reductions. Whilst it is unlikely that credits will ever equate with absolute precision to a tonne of CO2e, there are means to reduce perceptions of over-crediting, incorporating conservative values that may feasibly under-credit in some areas. Given the inherent uncertainty of emission reduction calculations, adopting such practices is the first step to ensuring quality, and slowly but surely reinstating trust in the market.

Next steps

Following these practices and being transparent in how values are obtained would increase the quality of cookstove projects. However, the reality is that increased robustness will also result in increased expenditure with potentially less reward. This is because developers will likely have to pay more to issue less credits, given the increased rigour of monitoring and reporting. And this is really the carbon conundrum. Having met with various representatives in the industry, it is apparent that they are aware of the perceived issues with these projects, but note that adopting more conservative measures could disrupt project finances to such an extent that it could entirely destabilise operations. This is because the price of carbon is currently so low that they would not be able to survive if issuing less credits, leading to concerns of a race to the bottom.

Given the precarious outlook for the sub-sector, it is apparent that carbon accounting concerns need to be addressed. Ultimately this will have to stem from the supply side, although we have already seen thresholds under implementation on the demand side. For example, Switzerland is paving the way for international emissions trading under Article 6.2, and has selected three cookstove projects in Ghana, Malawi, and Peru to contribute to its NDC. As part of this, the Swiss Federal Office of the Environment has suggested that it will only import emission reductions from this sector that have been calculated using the conservative 30% fNRB value, thereby setting a quality threshold. It is worth acknowledging that this threshold is still under consideration and may well change in light of the updated MoFuSS values being published by the UNFCCC.

Whilst this is an important first step, for markets to operate efficiently and at scale this quality must be linked to price. As such, developers need confidence that higher quality will afford higher credit prices. We have already seen this to some extent, with UpEnergy reporting sales of USD 52 per tonne for credits issued by their Community Carbon Efficient Cooking Programme, potentially as a result of positive buyer perceptions regarding the use of electric cooking technology (although this was found to only represent a fraction of distributed stoves, as discussed in our rating).⁸ And hopefully this can be further accelerated with the role of ratings agencies, which work to highlight project-specific risks, lending greater assurance of quality.

Conclusion

The takeaway is therefore that, yes, there are common problems in the Cookstove sub-sector, but these are by no means irreconcilable. In fact, we have already seen progression in cookstove methodologies, from infrequently monitored stoves made of mud to metered induction technologies built to last. Continued progression related to robust standards, conservative measurements, and transparent accounting will set the benchmark for quality in the Cookstoves sub-sector.

References

¹ World Health Organization. “Household Air Pollution Data.” Air pollution data portal, 2023. https://www.who.int/data/gho/data/themes/air-pollution/household-air-pollution.

² Bailis, Robert, Rudi Drigo, Adrian Ghilardi, and Omar Masera. “The Carbon Footprint of Traditional Woodfuels.” Nature Climate Change 5, no. 3 (2015): 266–72. https://doi.org/10.1038/nclimate2491.

³ IEA (2023), Tracking Clean Energy Progress 2023, IEA, Paris https://www.iea.org/reports/tracking-clean-energy-progress-2023

⁴ de la Sote et al., 2019 https://aaqr.org/articles/aaqr-17-11-ac3-0540.pdf

⁵ World Health Organisation, n.d. https://www.who.int/news-room/fact-sheets/detail/household-air-pollution-and-health

⁶ Clean Development Mechanism, 2023 https://cdm.unfccc.int/sunsetcms/storage/contents/stored-file-20231012184345703/MP92_EA07_Information%20Note_fNRB%20values_collated.pdf

⁷ Gill-Wiehl et al., 2023 https://assets.researchsquare.com/files/rs-2606020/v1/c2e6a772-b013-49f9-9fc4-8d7d82d4bebc.pdf?c=1678869691