An introduction to additionality in carbon projects

Here are some key takeaways

Additionality is a core concept to understanding and assessing quality in carbon markets. A project is considered ‘additional’ if its activities would not have been accomplished in the absence of the carbon project.

Standards bodies, methodologies, and compliance schemes often treat additionality as binary, but this approach misses nuance; additionality is better viewed as a spectrum.

BeZero’s data from more than 650 rated ex post projects exposes some broad trends in additionality risk by project type, but project-specific risks can still play a decisive role in a given credit’s risk.

Even before there were carbon rating agencies to help identify quality carbon projects, there were questions about how carbon market participants - from individuals looking to offset the carbon emissions of an annual vacation to corporations making larger investments in search of a bigger impact - could tell if the carbon credits they bought were making a real impact on the environment.

Many of those questions centred around how to tell if a project was ‘additional’. In other words, does a given project achieve climate benefits that would not have been realised without funding from carbon markets? While the infrastructure around carbon markets has matured quickly in recent years, questions about additionality remain key to understanding the quality of a carbon project, and it’s one of the three risk factors that BeZero Carbon evaluates when assigning a carbon rating.

What is additionality?

Many factors influence additionality, but the core question is: do the project’s activities avoid or remove CO2e emissions that would not have been avoided or removed without the carbon project?

Take the example of an avoided deforestation project, for which the project claims to use finance from the sale of carbon credits to offset the foregone profit the landowner could have realised by clearing the land.

If the land in question is severely threatened by logging, is owned by a logging company with strong financial incentives to clear the land, and no regulation or other policy prevents the landowner from cutting down the trees, then it’s likely the project is additional, because the trees probably would have been cut down if the project didn’t exist.

There is some discussion in carbon markets about the distinction between additionality and carbon accounting, and while the two are linked, they can be treated as distinct. BeZero’s approach to additionality asks: are the climate benefits driven by carbon finance, or would they have happened anyway? Our assessment of carbon accounting, on the other hand, examines the quantification of issuance: given our assessment of the additionality of the emissions-saving activities, is the number of credits issued consistent with the tonnes of emissions actually avoided or removed?

Our assessments of both factors depend on baselines, or what would have occurred if the project had not existed. Our view of additionality is informed by whether the project’s climate impact is additional compared to a reasonable baseline. Our view on carbon accounting considers the extent to which the project-reported baseline has been overestimated (among other factors).

How can I tell if a carbon project is additional?

The methodologies that guide the development of carbon projects outline mechanisms for projects to demonstrate additionality, and projects must have applied an additionality test or provide sufficient information on how it is deemed additional to be eligible for a BeZero Carbon Rating. This means that any verified ex post carbon credit will meet - or claim to meet - the criteria to demonstrate additionality as laid out by the relevant standards body or methodology. These tests typically treat additionality as a binary: projects either meet the standard and can issue carbon credits, or they do not.

Additionality tests by standards bodies

Standards bodies’ tests rely on threshold analysis; accreditation requires that a project has passed one or more tests set out by the methodology, rather than evaluating the extent to which it passes those tests.

Article 6 of the 2016 Paris Agreement on climate change lays out similar protocols for projects to demonstrate their additionality and participate in the Paris Agreement Crediting Mechanism, which enables the trade of verified credits.

This approach to additionality is fundamental to the functioning of a carbon market. Standards bodies must treat additionality as binary to issue whole units of carbon credits with equal assigned climate value; otherwise, the credits could never be traded or retired. You cannot issue or trade credits based on error bands or probabilities. However, it is more accurate to think of additionality as a spectrum, as we’ll discuss later.

Across the ex post projects rated by BeZero Carbon, we find at least 10 methods by which projects can claim additionality (see Table 1).

| Additionality test | Description |

|---|---|

| Common practice analysis | This method examines the pervasiveness of the methodology or technology applied by the project within the region and sector. Whilst not applicable to projects that qualify for ‘first-of-its-kind’ (see below), this method is typically concurrent with the other previously described methods described below for establishing additionality. |

| Identification of alternatives to the proposed project | This method evaluates whether a proposed activity can be substituted by any other feasible or credible activities. In addition to identifying alternatives, proponents may justify why these activities are not a viable alternative for the proposed project (such as financial and technical barriers) |

| Investment analysis | This step determines why the project is not economically or financially feasible without access to carbon credits. It applies either a simple cost analysis, investment comparison analysis or benchmark analysis. If either of the last two options to evaluate finances are applied, the proponents usually also complete a sensitivity analysis to confirm that their financial evaluations were robust. |

| Barrier analysis | Similar to the investment analysis, this step is undertaken to determine whether the project faces any significant barriers that prevent its implementation. In addition, this type of analysis also evaluates whether these barriers do not limit the activity of alternatives. Evidence to demonstrate that barriers are significant and/or do not hinder alternative activities can be substantiated by relevant legislation, industry norms, market data, etc. Examples of technical barriers examined could be the lack of skilled activity locally or adequate infrastructure to carry out the project whilst examples of ecological barriers (relevant for forestry or land use projects) may include soil quality and probability of unfavourable meteorological conditions. |

| Regulatory surplus | This test investigates the policy backdrop to a project’s activities. It requires project developers to assess whether any existing law, regulation, statute, legal ruling, or other regulatory framework directly or indirectly require GHG emission reductions or removals. |

| Positive list (Implicit) | An accredited-defined list of methodologies or activities that are granted automatic additionality if placed on this list. |

| First-of-its-kind analysis | This type of analysis sometimes falls under barrier analysis and determines whether the prevalence of prevailing practices hinders a project’s success. This has predefined limits in spatial scale or capacity. |

| Performance standard | Methodologies can have simplified requirements that grant additionality based on location (eg. Least Developed Countries) or qualitative demonstration of GHG-emitting baseline scenarios. |

| Methodology-driven (Implicit) | This test is a simpler combination of the common practice analysis and benchmark test (financial). It can incorporate local, policy and penetration components. |

| Activity-driven | This type of additionality test is new to Verra methodologies and requires project proponents to first demonstrate ‘regulatory surplus’ (see above). Following this, the project activities must be on the positive list where infrastructure is installed or distributed at zero cost to the end-user or be involved in any public schemes. This type of additionality test allows developers to bypass investment analyses. |

Table 1. Types of additionality tests commonly observed across BeZero-rated projects.

While the additionality tests employed by standards bodies set a baseline level of quality for projects that issue credits in the voluntary carbon market, their binary nature limits their usefulness for comparing project quality, and BeZero’s analysis has found that the number or type of additionality tests a project has passed isn’t a proxy for quality.

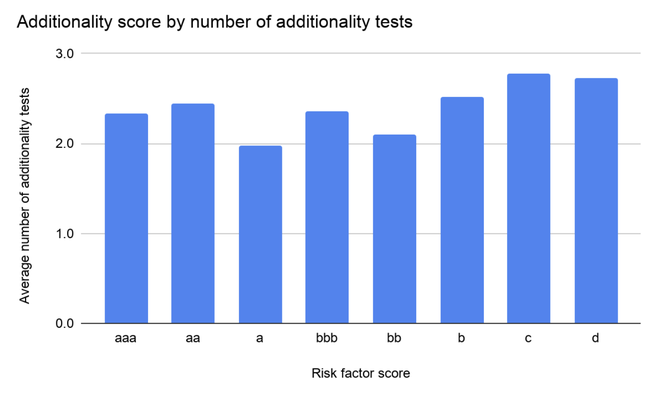

Figure 1 shows a simple analysis looking at the average number of additionality tests applied by projects with a given additionality risk factor score. The range between ratings is low, 0.8, with the highest 2.8 and lowest 2 tests per project covered in this analysis.

Figure 1. A rating distribution showing the average number of additionality tests applied, by BeZero’s additionaltiy score.

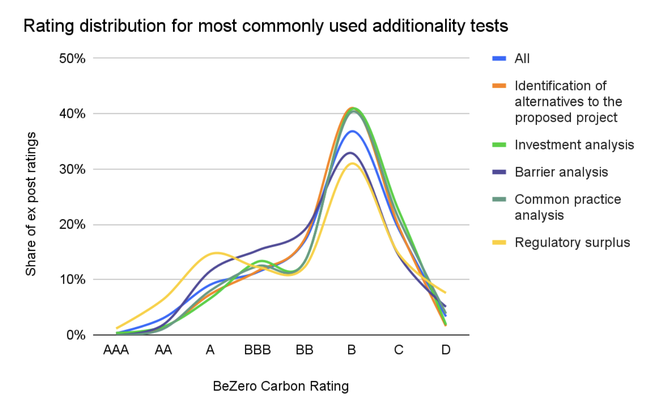

A similar picture emerges when assessing the distribution of ratings for the five most commonly used additionality tests across our dataset. Figure 2 shows a slight positive skew for those projects using the ‘regulatory surplus’ or ‘barrier analysis’ tests. But overall, each test shows a similar distribution to the total sample.

Figure 2. The rating distribution for projects using five of the most commonly used additionality tests as of January 2026.

How BeZero assesses additionality

BeZero Carbon does not apply binary tests or lists of approved activities to evaluate additionality. Instead, our ratings consider additionality as a spectrum, with scientists assigning each rated project a score to indicate the likelihood that the project is additional. The risk factor scores are on an eight-point scale, from highest (‘aaa’) to lowest (‘d’) likelihood of additionality. Our ratings scientists undertake their own research to holistically assess additionality, looking at factors across three broad categories, as outlined in our rating methodologies:

Activity analysis: evaluating the prevalence and effectiveness of project activities of a similar scale and in the same region as the project.

Financial analysis: assessing the accuracy and robustness underlying the project’s financial claim, barriers, incentives, and benefit-sharing structures.

Legal and policy risks: including policies or regulations that may be favourable to the project activity, including by mandating the activity or encouraging investment in such activities.

The ratings team starts by interrogating the appropriateness of the additionality tests applied by the standards body or required by the methodology, and identifying any limitations in the tools used by the developer to implement or evidence them.

Next, the team seeks to corroborate the data underlying a project’s additionality assessment using independent data sources, industry data, peer-reviewed research, and in-house expertise.

Our assessments go beyond self-reported project information and even consider factors occurring outside of the project’s boundaries that may influence its additionality. Inputs include the presence of global or national barriers to project delivery, the role of carbon finance in the overall revenue stream, and the effectiveness of policy instruments and governance for either pre-existing conservation or decarbonisation practices.

Crucially, each BeZero Carbon rating is based on deep, project-specific research and sector-level rating methodologies. There is no list of activities that we consider automatically additional (or automatically not additional), and even where our body of research has uncovered broad trends, we have also found projects that buck those trends.

Additionality risks across BeZero’s universe of rated projects

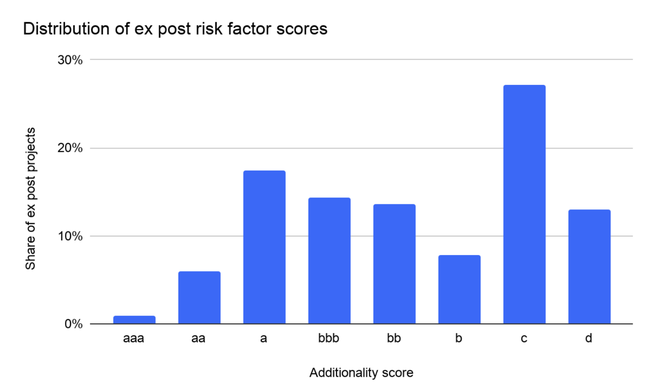

BeZero Carbon has rated more than 750 projects across dozens of project types, including 650 ex post projects, from which we pulled the data for this piece. The additionality scores for those projects range from ‘aaa’ to ‘d’ (see Figure 3).

Figure 3. The distribution of additionality scores for all ex post projects rated by BeZero as of January 2026.

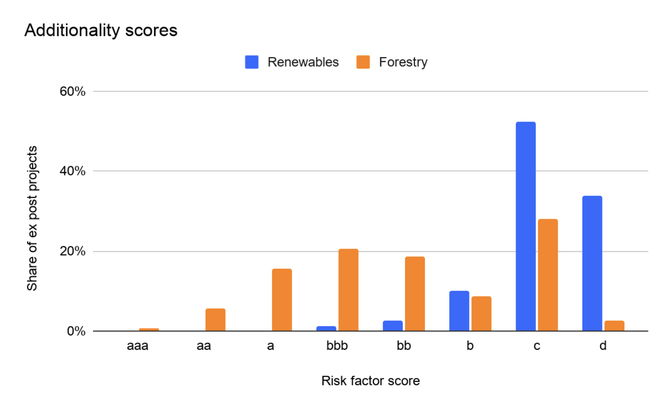

Splitting the ratings by sector can show a different picture. For example, Figure 4a shows the distribution of additionality scores in the Renewable Energy sector, where a large majority of rated projects have a ‘c’ or ‘d’ score, indicating a very low or the lowest likelihood of additionality. Figure 4b, on the other hand, shows that the additionality scores in the Forestry sector have a distribution that more closely resembles that of all rated projects.

Figure 4. The distribution of additionality scores for rated ex post projects in the Renewables sector (blue) and the Forestry sector (orange) as of January 2026.

Despite evidence of these sector-level trends, it would be wrong to assume that every project in, for example, the Energy Efficient Devices sector, where the median additionality score is ‘a’, has a stronger likelihood of additionality than every project in the Renewable Energy sector, with a median score of ‘c’. There are Energy Efficient Devices projects with a low or very low likelihood of additionality (‘b’ or ‘c’) and renewables projects with a moderately high likelihood (‘bbb’).

BeZero’s project-specific research has identified outliers across many of the sectors in our ratings coverage, proving that only deep, project-level due diligence can tell the real story of a carbon project.

Case study: small-scale hydro-electric dam projects

This comparison of two small-scale hydro projects (VCS 1716, an isolated mini-grid project in the Democratic Republic of Congo, and VCS 1241, a small-scale hydropower project in India) illustrates the importance of project-level additionality assessments.

Both projects are accredited by Verra, both are in the Renewable Energy sub-sector, and both are small-scale. However, VCS1716 has a ‘BBB’ BeZero Carbon rating and a ‘bbb’ additionality score, while VCS1241 has a ‘B’ rating and a ‘c’ additionality score. These rating differences were driven by our evaluation of the projects’ methods for determining additionality, the level of common practice for small-scale hydro projects in the relevant regions, and differing policy environments impacting the projects.

Additionality testing: VCS1716 uses the low rates of rural electricity access in the Democratic Republic of Congo (DRC) and the positive list to determine Additionality - this test is only suitable for projects that generate less than 15MW. Given the project’s small scale, we find this method for determining additionality appropriate. VCS1241, on the other hand, performs an investment analysis to gauge additionality against a benchmark internal rate of return. Our research suggests that using this type of Clean Development Mechanism investment analysis tool carries considerable risks.

Common practice: Our analysis finds that only 1% of the rural DRC population targeted by VCS1716 had access to electricity before the project began. Conversely, access to electricity in India was close to 80% when VCS1241 began.

Policy and regulatory environment: In the DRC, electricity development relies on external capital, and data indicate that infrastructure development is estimated to cost 30% of the nation’s GDP. In contrast, capital subsidies in India have been observed to routinely increase the internal rates of return on equity for small hydropower projects beyond benchmarks.

How can understanding additionality inform investment decisions?

Understanding the role of additionality in a project’s quality assessment is crucial for those looking to invest in carbon markets. Additionality is so important that a project’s inability to demonstrate additionality can be a limiting factor, making it ineligible to receive a BeZero Carbon rating. As noted above, standards bodies also require projects to pass additionality tests in order to issue credits.

Tracking broad trends can help focus early research by identifying project types most likely to be additional. Tools like BeZero Carbon’s AI assistant can help pick out the signals in the noise of our rated data set, which, paired with BeZero’s deeply researched reports for each rated project, can help to identify projects for investment, and our Pre-rating Scorecards can give a preliminary view of risk for projects that have not yet been rated.

Conclusion: Quality isn’t binary

Carbon markets tend to treat additionality as binary, giving the same credence to the claims made by all projects that issue verified credits, but BeZero’s analysis across hundreds of projects shows that the binary tests imposed by standards bodies and compliance markets do not adequately capture the variation in additionality that persists across virtually every sector in which projects are issuing credits. Expert, project-specific analysis and ratings are therefore key to identifying where individual projects fall on the spectrum of additionality risk, even for market actors who are aware of broad trends in quality for different project types.